If you’ve ever looked at your credit card statement and wondered why the balance seems to grow faster than expected, you’re not alone. The main reason behind this is something called APR. While it might sound technical, understanding APR can save you a surprising amount of money over time.

This guide breaks it down in a simple, practical way so you can not only understand how APR works but also calculate your own interest without needing complex tools.

What Is Credit Card APR

APR stands for Annual Percentage Rate. It represents the yearly cost of borrowing money on your credit card. In simple terms, it tells you how much interest you will pay if you carry a balance.

But here’s where many people get confused. APR is expressed annually, yet credit card interest is usually calculated daily. That’s why even a small balance can grow quickly if it isn’t paid off.

For example, if your card has a 24 percent APR, it doesn’t mean you’ll be charged 24 percent instantly. Instead, the issuer divides that rate into a daily charge and applies it to your balance every day.

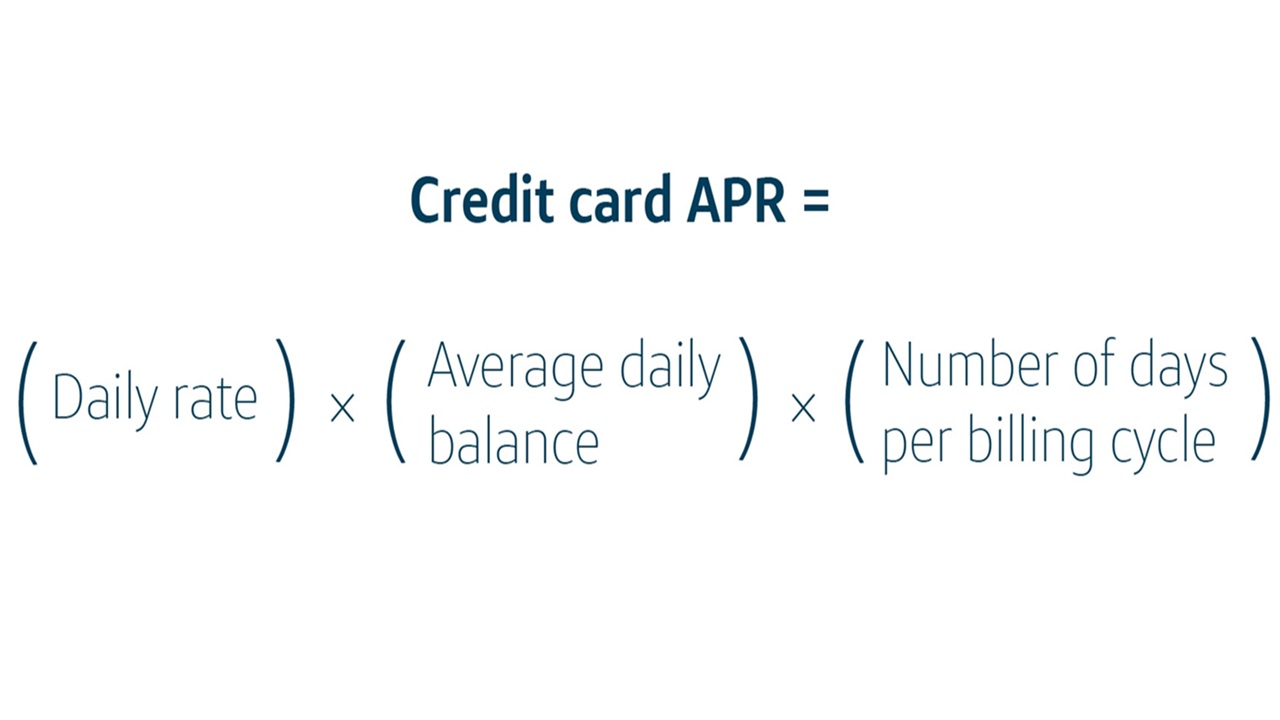

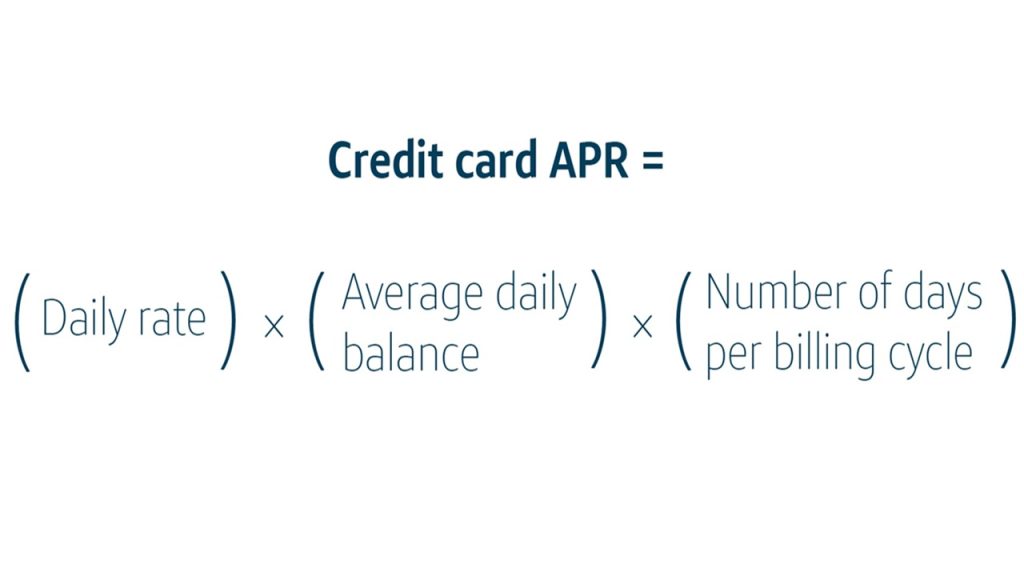

How APR Actually Works

To understand APR in a practical way, you need to look at the daily periodic rate. This is the real engine behind how interest builds up.

The formula is simple:

Daily Rate = APR ÷ 365

So if your APR is 24 percent:

24 ÷ 365 = 0.0657 percent per day

That number may look small, but it adds up quickly when applied daily to your balance.

Each day, the bank calculates interest based on your current balance. The next day, interest is calculated again, including the previous day’s interest. This process is known as compounding.

Types of Credit Card APR

Not all APRs are the same. Depending on how you use your card, different rates may apply.

Purchase APR

This is the most common type. It applies to everyday spending like shopping or paying bills.

Cash Advance APR

Usually higher than purchase APR. It applies when you withdraw cash using your credit card.

Balance Transfer APR

This applies when you move debt from one card to another. Some cards offer a lower promotional rate for a limited time.

Penalty APR

If you miss payments, your issuer may apply a much higher APR. This can significantly increase your debt.

Understanding which APR applies to your transactions helps you avoid unexpected charges.

Grace Period and Why It Matters

A grace period is the time between your billing cycle end and your payment due date. If you pay your full balance within this period, you typically won’t be charged any interest.

This is one of the easiest ways to avoid APR completely.

However, once you carry a balance beyond the grace period, interest starts accumulating daily. From that point, even new purchases may begin to accrue interest immediately.

Credit Card Interest Calculator Explained

You don’t always need an online tool to estimate your credit card interest. You can calculate it yourself with a simple method.

Here’s a step by step example:

Let’s say:

Your balance is 10,000

APR is 24 percent

Step 1: Find daily rate

24 ÷ 365 = 0.0657 percent

Step 2: Convert to decimal

0.0657 ÷ 100 = 0.000657

Step 3: Calculate daily interest

10,000 × 0.000657 = 6.57 per day

Step 4: Monthly estimate

6.57 × 30 ≈ 197.1

So, carrying a balance of 10,000 could cost you around 197 in interest per month.

This simple calculation gives you a realistic picture of how costly it can be to leave balances unpaid.

Why Minimum Payments Cost More

Credit Card Interest Calculator usually require a minimum payment each month. While it may seem manageable, paying only the minimum can stretch your debt over years.

Here’s why:

A large portion of your minimum payment goes toward interest, not the principal. That means your balance reduces very slowly.

Over time, you could end up paying double or even triple the original amount you spent.

This is why understanding APR is not just about knowledge. It directly affects how much money you keep in your pocket.

APR vs Interest Rate

Many people use these terms interchangeably, but there is a slight difference.

Interest rate refers to the cost of borrowing the principal amount.

APR includes the interest rate plus any additional fees associated with the credit card.

For most credit cards, the APR and interest rate are quite similar, but APR gives a more complete picture of the actual cost.

How to Lower Your Credit Card Interest

If you’re dealing with a high APR, there are practical ways to reduce its impact.

Pay your full balance whenever possible

This eliminates interest entirely during the grace period.

Make more than the minimum payment

Even small extra payments can reduce your principal faster.

Look for lower APR cards

Balance transfer cards with promotional rates can help manage debt.

Improve your credit score

A better score can qualify you for lower APR offers in the future.

Avoid cash advances

These usually come with higher APR and no grace period.

Real Life Example That Makes It Clear

Imagine two people using the same credit card.

Person A pays the full balance every month.

Person B carries a balance of 10,000 at 24 percent APR.

After one year, Person A pays zero interest.

Person B could end up paying over 2,000 in interest alone.

The difference isn’t income or spending habits. It’s how they manage APR.

Common Mistakes to Avoid

Ignoring APR while choosing a credit card

Low rewards don’t matter if the APR is too high.

Missing payment due dates

This can trigger penalty APR and late fees.

Assuming interest is calculated monthly

It’s calculated daily, which makes a big difference.

Relying only on minimum payments

This increases long term debt significantly.

Final Thoughts

Credit Card Apr Calculator might seem like just another number on your statement, but it has a real impact on your finances. Once you understand how it works and how to calculate it, you gain control over your spending and debt.

The key takeaway is simple. If you can, pay your balance in full each month. If not, use the interest calculation method to stay aware of what you’re being charged.

That awareness alone can change the way you use credit cards and help you avoid unnecessary costs in the future.

Understanding APR isn’t about being a finance expert. It’s about making smarter decisions with the money you already have.

Leave a Reply